What looked like a potential tidal wave for the architecture industry—one that would wipe out the relative economic gains of the past year—has turned out to be just another ripple in a still uncertain marketplace. In January, the Architecture Billings Index saw one of its steepest declines in months, but those losses were all but erased in February, according to numbers released by the AIA today.

That February has somewhat reversed such a precipitous drop—when inquiries fell the furthest they have since October 2008, when the market collapsed—is a promising sign, though it also means the slight gains seen in the index last fall were not yet signs of a permanent recovery.

“It’s not positive yet,” AIA Chief Economist Kermit Baker said of the billings index, “but I anticipate that in the coming months. It may not actually be supported by the numbers directly, but there are signs in the wider economy that we should be headed in the right direction.”

Billings for February rose 2.3 points to 44.8, nearly besting a 2.9-point loss the month before. A reading above 50 means billings are rising while one below means they are falling; the greater the spread, the greater the gains or losses. So while billings did increase in February, they are still in declining territory—things have gotten better instead of worse, but they are by no means good.

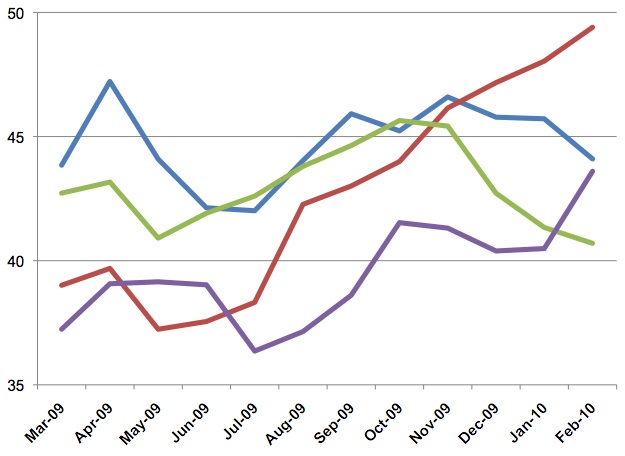

There are some surprising exceptions, however. The Midwest region has been on a tear the past few quarters, rising to 49.4 in February, the highest reading for any region since the recession began. Baker attributes this to strong manufacturing performance in the region. “People are increasingly looking domestic for such work,” Baker said.

The West has also made a comeback—of which Baker is more skeptical because of the continued troubles of California’s state budget, even as housing has stabilized somewhat. From a low of 36.4 in July, the West has risen to a comparably robust 43.6.

It is not all good news for the regions, though, as the Northeast has slipped slightly to 44.1 since its most recent high of 46.6 last November. And the South, which had been on the rise throughout much of last year, has fallen to 40.7 in February from a recession-best of 45.6 in October. “Regionally, I would have guessed the south would have carried us out of the recession, with its oil and agricultural commodities,” Baker said. “But the region is so diverse, and it has Florida in there and Atlanta hasn’t been doing so well, so that’s been a factor.”

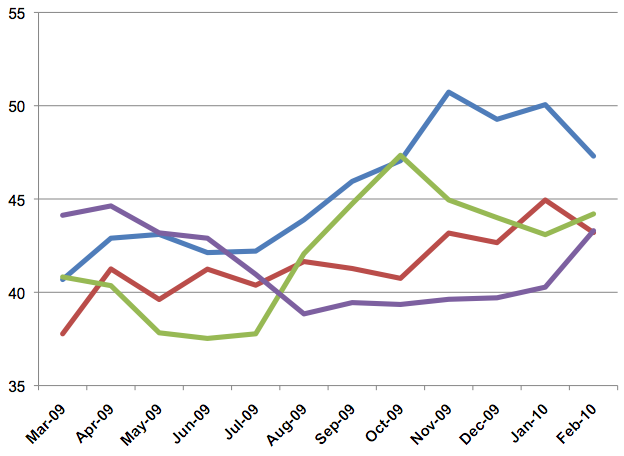

Billings by sector have seen a similar rollercoaster. Multifamily housing has been especially strong, driven by gains across the housing market, and it was the first of any indicator to break the 50 threshold, reaching 50.7 in November. That said, it has sunk to 47.3 in February, from 50.1 the month before, with Baker waiting on a two-to-three month gain to declare anything decisive. While still low, mixed-use development has posted a slight comeback, rising to 43.3 from 40.3 in January, breaking a trend going back to August when the sector hovered in the high 30s.

Institutional work gained in February to 44.2 from 43.1 the month before, though that was following a fall from 47.3 October. And despite the success of manufacturing in driving the Midwestern economy, it has yet to have an impact on actual manufacturing facilities, as the commercial-industrial sector—which has also been hampered by problems in the office market—still struggles. The sector fell to 43.2 in February from 44.9 in January, though it has also seen some gains since a low of 39.6 last May.

“If people are not thinking about hiring back their workers yet, they’re certainly not going to be sitting down with their architects to work on capital projects or expansion plans,” Baker said. He does expect job growth by the second quarter, however, based on historical analysis looking at the past four recessions—much as the AIA predicted earlier this year. “If this recession is like past ones, I fully expect us to be back to work by the summer,” he said.